A major focus of Karl Seidman’s work is knowledge and tool development for economic and community development practitioners. This section highlights and connects to key publications and resources from this work in three fields.

Economic Development Finance

This textbook provides a comprehensive and in-depth presentation of the basics of business and real estate finance; private, public, and community financial institutions; and policies and tools for financing business enterprises and economic development projects. The treatment of policies and program models emphasizes their applications and impact, key design and management issues, and best practices. A separate section addresses critical management issues for development finance programs: program and product design, the lending and investment process, and capital management. Order from Sage Publications Here or Amazon Here

Financing Community Development

This slide deck details the United States community development finance system through a framework of project financing, financial intermediaries and local finance systems using Boston and Detroit as case studies. It includes an overview of the different tools and capital stacks to finance affordable housing, commercial real estate and small businesses, project and intermediary case studies and descriptions of citywide finance systems. Download UVA Class Slide Deck

Financing Economic Development Course

Karl Seidman developed and taught this graduate level course for 25 years. Visit MIT’s Open Courseware site for 11.437 Financing Economic Development for detailed course information including the syllabus, lecture slides, readings and other materials.

Photo courtesy of Edmonton Economic Development Corporation on Flickr. CC BY-NC-SA.

Learn more about our Development Finance Experience

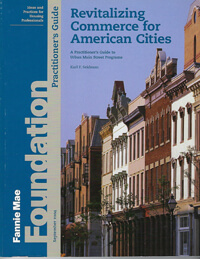

Revitalizing Commerce for American Cities: A Practitioner’s Guide to Urban Main Streets

This guide, prepared for the Fannie Mae Foundation, addresses how to apply and adapt the Main Street commercial revitalization model developed for small communities to urban commercial districts. It draws on practitioner experience from seven Main Street programs in three cities with specific action steps to implement and expand upon the four-point Main Street approach. Detailed case studies of four urban Main Street districts are included. Download this publication here.

Inner City Commercial Revitalization Literature Review

This literature review prepared to inform the Practitioner’s Guide Urban Main Streets provides a framework and summary of research on the varied strategies and tools used to revitalize inner city commercial areas. Download this publication here.

Revitalizing Urban Main Streets Course

Karl Seidman developed and co-taught this graduate level course which prepared over a dozen plans for commercial districts in Boston and New Orleans. Visit MIT’s Open Courseware site for 11.439 Revitalizing Urban Main Streets for detailed course information including the syllabus, lecture notes, reading and sample plans.

St. Roch Market, pictured here post-Hurricane Katrina, is seen as the centerpiece of the St. Claude Avenue Main Street District. The market’s fate is seen as mirroring the fate of the surrounding area. (Image courtesy of quebella on flickr.)

Learn more about our Commercial District/Corridor Revitalization Experience

With climate change a growing environmental and economic challenge, it has becoming increasingly important to incorporate carbon reduction and environmental sustainability goals as core economic development outcomes. Working with MIT CoLab, Karl Seidman led the Green Economic Development Initiative (GEDI) which brought together leading economic development practitioners in dialogue about how to move the field toward integrating environmental and equity goals into economic development work.

Through this work, these practitioners prepared Transforming Economic Development which makes the case for, and details strategies and case studies for Triple Bottom Line economic development that addresses environmental sustainability and equity as core components of economic development.

GEDI partnered with local government agencies on “action research” projects to develop energy efficiency market transformation strategies for commercial buildings in each agency’s region. The Energy Efficiency Market Transformation Guidebook and accompanying resources draw on this work to present how communities can formulate a commercial energy management market transformation strategy and suggests common policies, approaches, and tools to deploy such strategies. It is intended to support your community’s ongoing economic development and environmental initiatives.

Download the Energy Efficiency Market Transformation Guidebook

Visit the Energy Efficiency Market Transformation Strategy web page to view and download city strategy reports and other resources here

A third GEDI project looked at the growing use of green storm water infrastructure and how these investments can advance equitable economic development outcomes. MIT GEDI – Green Infrastructure and Economic Development.

ABOUT

Karl F. Seidman Consulting Services advises clients on the planning, implementation, and evaluation of economic development strategies, policies and programs and on the analysis, planning and financing of real estate development projects.